What If I Am Struggling to Make Mortgage Payments?

Key Highlights

- Missing mortgage payments can quickly reduce your credit score and lead to the foreclosure process, risking your homeownership.

- Financial hardship due to job loss or medical emergencies can make mortgage payments unmanageable, but early action with your mortgage lender is crucial.

- Options such as loan modification, forbearance, or payment deferral can help reduce monthly payment amounts and prevent mortgage default.

- Refinancing or selling your home may offer alternative relief if regular payments remain unaffordable.

- Licensed professionals like housing counselors can guide you through debt relief options and help you plan for sustained financial stability.

Introduction

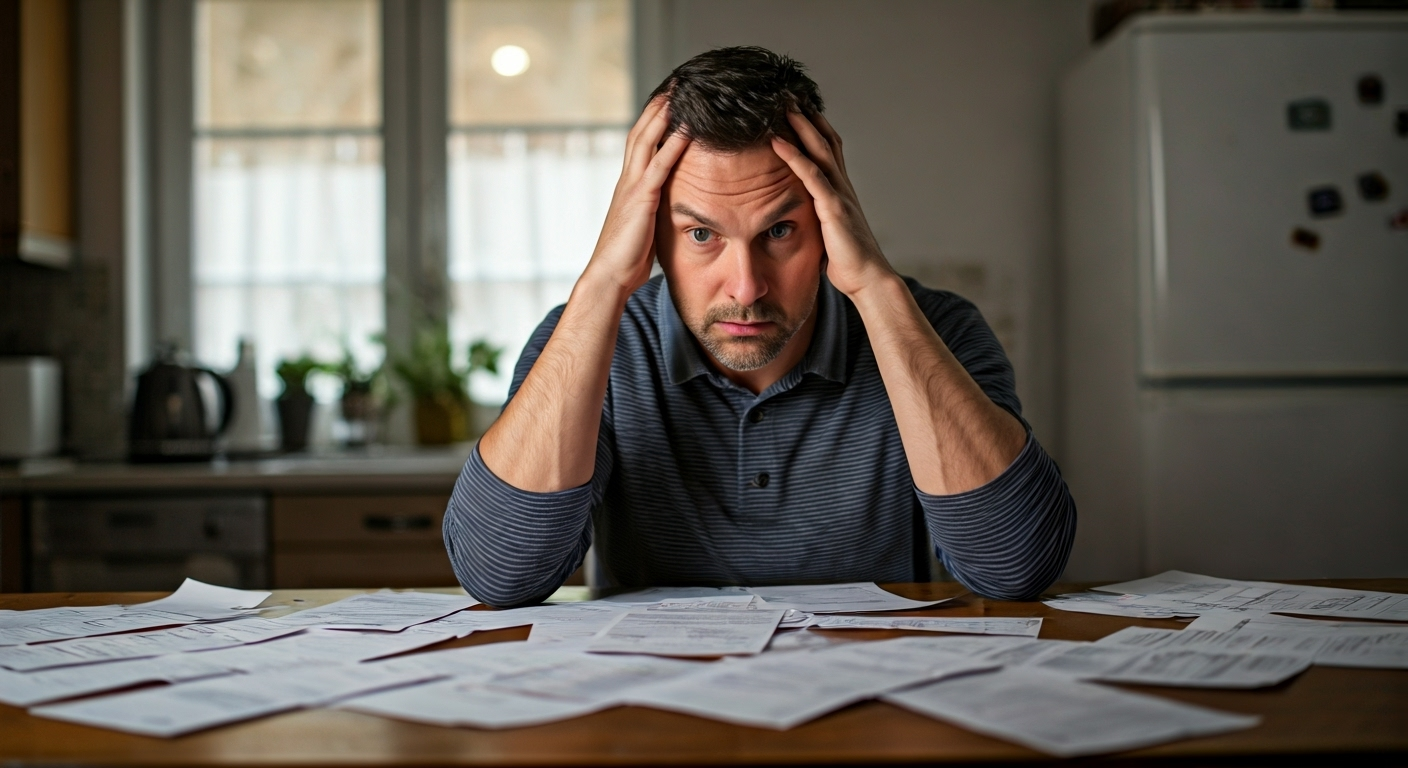

Finding it hard to keep up with mortgage payments can be tough. Things like high interest rates or a loss of income can make it even harder. When you miss payments, it can hurt your credit score. If you do not act, this can also lead to your home being taken away in a foreclosure. The good news is that there are lenders and programs that help you avoid mortgage default. No matter if you are facing short-term problems or long-term financial difficulties, you do have options. There are ways to deal with missed payments and lower the stress. Let’s look at what you can do to tackle missed mortgage payments before things get worse.

Understanding the Impact of Missed Mortgage Payments

Falling behind on mortgage payments can cause a lot of problems. When you make missed payments, even if you think it is no big deal at first, it can hurt your credit score in a big way. Credit bureaus keep records of late payments. This information can stay on your credit report for up to seven years. Because of this, you may find it harder to get credit or loans in the future.

Falling behind on mortgage payments can cause a lot of problems. When you make missed payments, even if you think it is no big deal at first, it can hurt your credit score in a big way. Credit bureaus keep records of late payments. This information can stay on your credit report for up to seven years. Because of this, you may find it harder to get credit or loans in the future.

If you keep making missed payments, you can face mortgage default. This means that your lender might start the process to take away your home. Foreclosure is serious, and you could lose your property. So, it is important to understand how missed payments can impact you. The first thing to do is see how serious this is and start looking for ways to fix the problem.

How Missing Payments Affects Your Credit Score

Missing mortgage payments can hurt your credit score right away. If you miss a payment for more than 30 days, credit bureaus like Equifax and TransUnion will be told. This will bring your score down. Late payments stay on your credit report for many years. This can make it hard for you to get loans, another mortgage, or a line of credit when you need them.

Making regular payments is key for keeping a good credit score. If you stop making regular payments, your risk goes up. It also means you have less freedom with your money if an emergency happens. Showing payment consistency tells lenders that you are reliable.

If you have trouble with your mortgage payments, act fast. Reach out to your lender before missed payments show up at credit bureaus. You can ask to make a new plan. This can help you avoid bigger problems like foreclosure, and it may stop your whole credit profile from being hurt.

Consequences of Delinquency and Foreclosure in the U.S.

Delinquency on mortgages happens when you are late on a payment by more than 30 days. At this point, your mortgage lender will usually charge late fees. They will also tell credit bureaus about the missed payments, which can make your financial problems worse. Things like job loss or having your income go down can lead to this situation.

If you keep missing payments and do not solve the problem, the foreclosure process could start after 120 days. Foreclosure means you can lose your home. It lowers your credit score and makes it hard for you to get back on your feet. Lenders will also take and auction off the property to get back the money you owe.

The risk of foreclosure shows why you need to act fast. If you talk with your mortgage lender or housing counsellors right away, you can make a new plan or find a solution. This could help you keep your home and stop the foreclosure process

.

Immediate Steps to Take If You’re Struggling

If you find your financial situation getting hard and you can’t keep up with mortgage payments, you need to act fast. Look over your expenses so you can find ways to cut back. Try to work on reducing your debt for now so things get a bit easier.

If you find your financial situation getting hard and you can’t keep up with mortgage payments, you need to act fast. Look over your expenses so you can find ways to cut back. Try to work on reducing your debt for now so things get a bit easier.

You should contact your mortgage lender as soon as you see a problem. Talk to them about what options they have to help you. Doing this early can help you stop a formal foreclosure. The lender can work with you on things like new payment plans or even delays that fit your needs.

Assessing Your Financial Situation

The first thing you need to do if you have issues with your mortgage payments is to look at your financial situation. Make sure you know about all your unsecured debts, monthly expenses, and the income you have coming in. When you make a quick overview of your cash flow, it can help you see why keeping up with your payments feels hard.

Focus first on the basics, like credit card payments and ways to cut down on any additional debt. If you stop spending on things you do not need, you can use more of your money to pay your mortgage. If you know your budget well, you will be ready to talk about all the possible solutions.

Try to stay steady. Look into things like debt consolidation or finding ways to work out new deals on how you pay what you owe. Using this kind of plan, you can avoid long-term money problems and lower the risk of mortgage default in the future.

Contacting Your Mortgage Lender Early

Open communication is very important when you have missed payments. Most mortgage lenders want to work with you and not go for foreclosure right away. Talking to them early shows that you are taking action and that you are honest about your financial hardship.

Many lenders have free meetings for homeowners who are having trouble with regular payments. This helps you know what choices you have. You need to face the problem before your payments are marked as default. Lenders care more about working with you than going straight to court.

If you have missed payments, reaching out early helps you find ways like lower regular payments or plans to pause payments for a while. When you act quickly and stay open with your lender, you protect your credit score. You also stop bigger problems for your loan and make it easier to keep good lending relationships.

Exploring Options to Modify Your Mortgage

Mortgage modifications are made to help lower how much you pay or to change loan details so it is easier to afford. There are programs like payment deferral or making your loan last longer. These give you some extra time to deal with money problems for now.

You should talk with your lender to look at what you can do, like adding your missed payments to what you already owe. Another option is to ask about changing your interest rates. These changes can fit better with what you are able to pay and help you keep your house safe.

Loan Modification Programs

Loan modification programs help by making changes to your mortgage agreement. These programs often lower interest rates. This makes your monthly payment smaller and easier to handle. People who are having a hard time with money can get help from this.

You can get a longer time to pay, which brings your monthly payment down. This can help if you need to stick to a tighter budget. Making payments over a longer time can keep you in your home even when things are tough.

When you get a new agreement, the mortgage principal or any past amount owed gets spread out over more years. This helps lower your stress now. At the same time, your payment stays in line with the lender’s rules.

Forbearance and Payment Deferral Options

Forbearance lets you pause or cut down your payments for a short time. It can be a good choice if you have some quick money troubles. Payment deferral means you will move your missed payments into the future. These payments are split across the rest of your loan.

These ways help keep people in their homes if they need help for a short while. But, you should know that interest charges will keep adding up while you are not paying. This means the total cost of your mortgage amortization may be higher in the end.

| Option | Key Details |

|---|---|

| Forbearance | Payments are paused or you pay less for now |

| Payment Deferral | Move missed payments to later in your loan |

| Amortization Extension | Make the payback time longer. Your monthly payment gets smaller |

Alternative Solutions to Prevent Foreclosure

When changes to your loan do not work, you can try to refinance or sell your home instead. Refinancing may get you a lower interest rate or let you pay your loan back over a longer time. This can help lower what you have to pay every month.

If you sell your home, you use any money left, called equity, and stop missed payments from piling up. Both of these ways can help keep your money in order and help you avoid late fees and the costs that come with foreclosure.

Refinancing Your Home Loan

Refinancing changes the way your loan works to help fit where you are now with your money. Picking lower or fixed interest rates can help give you stability. This is good when your loan has variable rates that can go up and cause you stress.

Many people choose refinancing when they face financial hardship. It helps you keep up with payments in fixed situations. You may even see your monthly mortgage payments go down for a while.

This is a way to help protect you against more debt and rising interest rates. It also helps your money health to get better with time, as you save every week from lower interest.

Selling Your Home to Avoid Foreclosure

Selling your property early can help you avoid home seizure and stop money problems that happen due to foreclosure. If the amount you still have to pay on your mortgage balance is higher than what you can manage, and stress with money goes on, putting your home up for sale protects you from bigger problems down the line.

When you have built up a lot of home equity, you have other choices. You can downsize to a smaller place to get free from a big mortgage for good. Or, you could make extra payments to clear some of the debt fast. This can give you a better chance for quick money recovery and make the situation better.

If things get worse, selling your home right away can stop extra dollars being added on through interest because of late payments. It helps wipe away the money you owe quickly and stops the problem from going on longer.

Seeking Professional Help and Support

Getting through financial difficulties can be tough. At times like this, it helps to talk to licensed insolvency trustees or HUD-approved housing counselors. They can help you see what choices you have if you missed payments on your mortgage. These professionals can talk with you about how to get a deferral on your payments and may help you lower the worry about missed payments.

Having a free consultation is a good step. In this meeting, they might show you debt relief choices like a consumer proposal or a consolidation loan. These could help steady your financial situation. If you take quick action when things are hard, you can lower the risk of mortgage default and also help protect your credit score. Acting fast when there is trouble can make a big difference for you and your family.

Consulting with HUD-Approved Housing Counselors

Talking with HUD-approved housing counselors can help you with money problems about your mortgage payments. These experts give you important advice about many debt relief options, such as mortgage payment deferral or loan consolidation. When you have a free consultation, you can talk about your financial situation and look at different ways to lower the chances of missing your mortgage payments. Their knowledge helps you understand the terms of your mortgage and make a plan to take control of your monthly payment. This way, you can avoid late fees and mortgage default.

Conclusion

Handling mortgage payments can be tough, especially when money is tight. If you have problems with your financial situation, you can look at options like mortgage payment deferral. It may also help to talk with a HUD-approved housing counselor. These steps can make things clearer for you. Acting quickly can lower the risk of mortgage default and keep your credit score safe. Remember, there are people and tools set up to help you. You can get the right debt relief options for your needs. Take the first step and work towards a better money future today.

Click Cash Home Buyers

Looking at options with click cash home buyers can help if you are struggling to make your mortgage payments. These buyers move much faster than the usual way of selling a home. When you work with them, you often skip slow steps and get to a quick deal. This can take away the worry of missed payments and ease stress from financial difficulties. With this choice, you may avoid the risk of falling behind and even stop foreclosure. It is a way to sell fast, get out from your debt, and start fresh. Sometimes, this new beginning is only a click away call click cash home buyers 209-691-0102

Frequently Asked Questions

Can I skip a mortgage payment without penalty?

Skipping a mortgage payment is usually not a good idea. It can lead to fees or hurt your credit score. Some lenders may help you during tough times by allowing forbearance. It is best to talk to your lender before you miss any payments. Missed payments can have a big effect on your credit score, so always ask for help if you need it.

What government programs can help if I’m behind on my mortgage?

Government programs like the Home Affordable Modification Program (HAMP), FHA-insured loans, and different help plans run by states can help you if you are late on mortgage payments. You should talk to your lender to see if you can get these options and learn how to apply for them.

How many missed payments before foreclosure starts?

Usually, foreclosure starts when there are three to six missed payments. But, this number can be different depending on where you live and what your lender decides. It is important to talk with your lender as soon as you can. By doing this, you may find a way to work things out. You can also stop the problem from getting worse if you talk early.

Will selling my home hurt my credit?

Selling your home can change your credit. This is true if you still have a mortgage balance. If you do a short sale or your home goes into foreclosure, there can be bad marks on your credit report. But if you sell your home in a normal way without money problems, it usually has little effect on your credit.

What should I do if I can’t afford my mortgage long-term?

If you find that you can’t pay your

for a long time, there are some options to look at. You can try a loan change, refinance, or talk to housing advisers who are approved by HUD. They can help you find programs that fit your needs or talk with your lender to help make your payments easier to handle.